Abstract

Portfolio rebalancing is the process of bringing the different asset classes back into proper relationship following a significant change in one or more assets. You return your portfolio to the proper mix of stocks, bonds, cash or other assets when they no longer conform to your plan/limits.

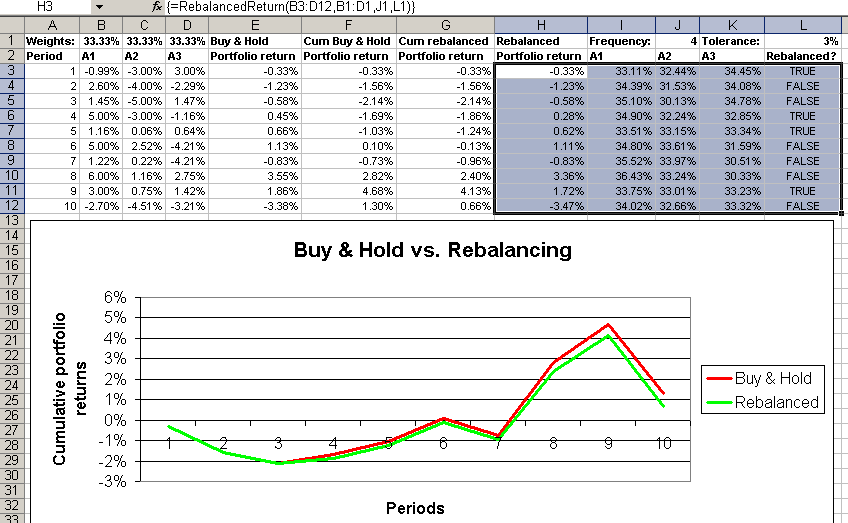

An example:

Appendix – sbRebalancedReturn Code

Please read my Disclaimer.

Option Explicit

Const CMaxDouble = 1.79769313486231E+308

Function sbRebalancedReturn(rARM As Range, _

rIWV As Range, _

Optional ByVal lRF As Long = 0, _

Optional dDT As Double = CMaxDouble) As Variant

'RebalancedReturn calculates balanced returns for a

'portfolio with given

'rARM - asset return matrix (columns show different

' assets, rows show returns per asset over time)

'rIWV - initial weight vector for the assets

'lRF - rebalancing frequency (in time steps = rows)

' If lRF > 0 then each lRF time step rebalancing

' will take place

' If lRF = 0 then no rebalancing will take place

' If lRF < 0 then each -lRF time step after last

' rebalance portfolio will be rebalanced again

'dDT - drift tolerance %, if any asset has drifted by

' by more than dDT (relative measure) then the

' portfolio will be rebalanced AND the internal

' rebalancing frequency count will be reset

'The output matrix shows portfolio returns % in first

'column, then end-of-period asset weights and finally

'boolean output values in last column, showing whether

'a rebalance happened.

'This function has been inspired by Andreas Steiner's

'similar function.

'Source (EN): http://www.sulprobil.de/sbrebalancedreturn_en/

'Source (DE): http://www.berndplumhoff.de/sbrebalancedreturn_de/

'(C) (P) by Bernd Plumhoff 19-Mar-2011 PB V0.2

Dim i As Long, j As Long, k As Long, n As Long, m As Long

Dim bDrifted As Boolean, bForceRB As Boolean

n = rARM.Rows.Count 'Number of observations

m = rARM.Columns.Count 'Number of assets

If m <> rIWV.Columns.Count Or _

rIWV.Rows.Count <> 1 Then

sbRebalancedReturn = CVErr(xlErrValue)

Exit Function

End If

ReDim w0(1 To m) As Double, x(1 To m) As Double

ReDim r(1 To n, 1 To m) As Double

If lRF = 0 Then lRF = n

If lRF < 0 Then

lRF = -lRF

bForceRB = True

Else

bForceRB = False

End If

ReDim vR(1 To n, 1 To m + 2)

For i = 1 To m

x(i) = rIWV(i)

w0(i) = x(i)

For j = 1 To n

r(j, i) = rARM(j, i)

Next j

Next i

k = 1

'Model rebalancing tolerance

For i = 1 To n

If bDrifted And bForceRB Then k = i

'Calculate period start weights

vR(i, m + 2) = (i - k) Mod lRF = 0 Or bDrifted

If vR(i, m + 2) Then

For j = 1 To m

x(j) = w0(j)

Next j

Else

For j = 1 To m

x(j) = vR(i - 1, 1 + j)

Next j

End If

'Calculate portfolio return

For j = 1 To m

vR(i, 1) = vR(i, 1) + x(j) * r(i, j)

Next j

'Calculate period end weights & check for drift

bDrifted = False

For j = 1 To m

vR(i, 1 + j) = x(j) * (1# + r(i, j)) / (1# + vR(i, 1))

bDrifted = bDrifted Or Abs(vR(i, 1 + j) - w0(j)) > dDT

Next j

Next i

sbRebalancedReturn = vR

End Function

Download

Please read my Disclaimer.

sbRebalancedReturn.xlsm [25 KB Excel file, open and use at your own risk]